Why the Bull Market Still Has Legs

THE MARKETS

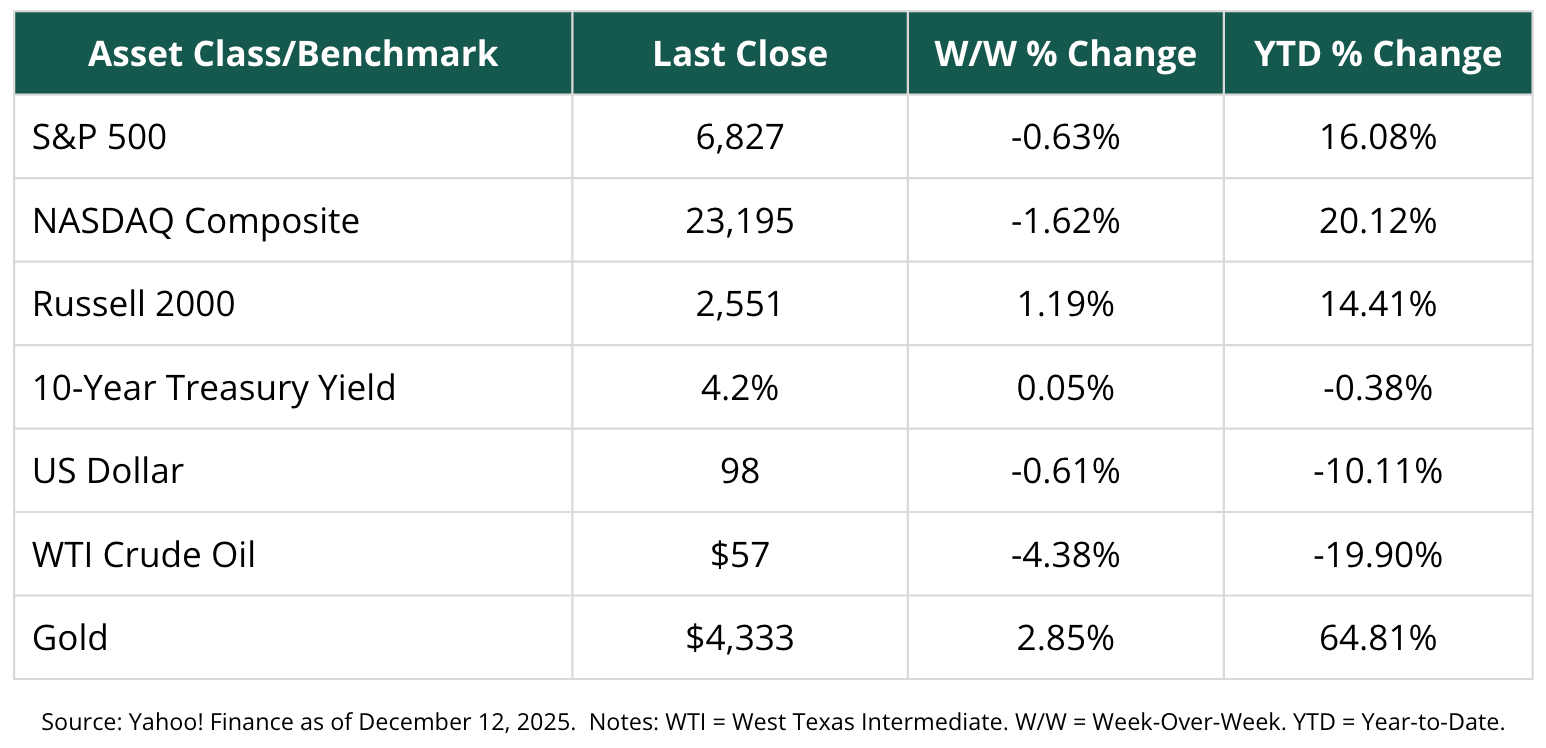

Markets were mixed this week as investors digested strong year-to-date gains against near-term consolidation. Large-cap equities pulled back modestly, while small caps showed relative strength. Treasury yields edged higher, the U.S. dollar weakened further, and commodities diverged—Oil continued to slide while gold surged to new highs.

Despite the week’s uneven tone, the broader trend remains constructive. Equity leadership is expanding, financial conditions are easing, and investor sentiment is still cautious—an environment that has historically supported higher prices over time.

HIGH QUALITY DESERVES A HIGH PRICE

“Price is what you pay. Value is what you get.” — Warren Buffett

Since early January, WCG’s Investment Strategy Committee (ISC) has expected a double-digit stock market return, led by pro-cyclical, economy-sensitive sectors—most notably information technology and consumer discretionary. The surge in those sectors since the April low has reinforced our risk-on posture.

What’s next? If the mid- to late-1990s provide a roadmap for “tech mania 2.0,” U.S. mega-cap technology stocks may continue to command a dominant share of investor portfolios. Strong fundamentals remain the primary driver of performance, which is why we are staying overweight and why we believe technology could help propel the S&P 500 toward 8,500 by 2026.

Concerns about valuation, market concentration, and narrow leadership are understandable. However, historical context matters. From the release of Netscape Navigator in the mid-1990s to the market peak in 2000, technology stocks rose roughly 925%. Since the launch of ChatGPT, technology stocks have increased approximately 156%—a meaningful gain, but far from late-1990s extremes.

While risks are rising, they remain materially lower than during prior speculative cycles. In our view, investors willing to pay for durable growth—strong revenues, high margins, and accelerating earnings—may still find opportunities ahead.

“The four most dangerous words in investing are: ‘This time it’s different.’” — Sir John Templeton

A CATCH-UP PHASE FOR THE BROADER STOCK MARKET

If history is a guide, technology leadership does not preclude broader participation. Rather than signaling an imminent collapse, today’s environment may represent a catch-up phase for other sectors, powered by technological efficiency and productivity gains.

Despite common misconceptions, technology valuations remain within a reasonable range. The sector typically trades at a premium to the broader market due to superior earnings growth. Current valuation levels, while elevated, are consistent with past expansionary periods—particularly when margins and revenue growth remain strong.

The bottom line: As long as earnings continue to rise, interest rates trend lower, and pessimism remains elevated, risk assets—especially equities—can continue to grind higher.

THOUGHTS ON THE OUTLOOK

Just a few weeks ago, we questioned whether next year’s market performance might cool after three consecutive years of strong returns. That outcome remains possible, and a deeper analysis has shifted our outlook.

Market participation is broadening beyond the largest names. Capital expenditures—particularly in technology and artificial intelligence—are accelerating. Monetary policy is becoming more accommodative. Most importantly, the market is exhibiting a rare mix of strong fundamentals, improving momentum, subdued sentiment, and ample dry powder on the sidelines.

Technology-driven productivity gains are likely to be deflationary over the long run, easing pressure on interest rates while supporting earnings growth. In that environment, diversified portfolios—across sectors, styles, and factors—remain best positioned.

HUMAN INTEREST: PERSPECTIVE MATTERS

It’s often said that markets test patience more than intelligence. Periods when valuations feel uncomfortable and headlines feel ominous are frequently the same moments when long-term returns are being quietly built. Staying focused on quality, discipline, and evidence—not noise—is still one of the most underrated investment advantages.

“Investors are better served by emphasizing long-termism and de-emphasizing short-termism.’” — Talley Léger

INTERESTING FACTS AND FIGURES

Did you know that:

The average human attention span is now estimated to be shorter than that of a goldfish, according to multiple behavioral studies.

Productivity gains from past technological revolutions—electricity, automobiles, computers—often took decades to fully show up in the economic data.

Contrary to popular belief, over 90% of the world’s trade still moves by ship, highlighting how physical infrastructure underpins the digital economy.

Best Regards,

Andrew Zittell

Yerba Buena Financial Partners

Andrew Zittell, CLU®, ChFC®, AIF®, RFC® is a registered representative with, and securities offered through LPL Financial, Member FINRA/SIPC. Investment advice is offered through WCG Wealth Advisors, LLC, a registered investment advisor. The Wealth Consulting Group, WCG Wealth Advisors, LLC, and Yerba Buena Financial Partners are separate entities from LPL Financial.

The LPL Financial registered representative(s) associated with this website may discuss and/or transact business only with residents of the states in which they are properly registered or licensed. No offers may be made or accepted from any resident of any other state.

Sources: Bloomberg, FactSet, S&P Global, YCharts, WCG, Historical market data and valuation comparisons as of 12/12/25.

Disclosures:

- Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield. (118-LPL)

- The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly. (102-LPL)

- The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index. Indexes are unmanaged and cannot be invested in directly. (112-LPL)

- The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors. (122-LPL)

- There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)